Monday May 9 Daily Market Primer

Stocks

rose in the US Friday after opening down, as the disappointing jobs number that

failed to impress the market led investors to conclude that it will be even

harder for the Fed to raise interest rates. The market based odds of

a June increase fell to just 2 percent after the jobs report. Payments

processor Square got crushed (-22%) on Friday after reporting that their small

business loan program is off to a very slow start.

I

simplified the returns table by taking off a few of the individual

countries, and I added the US 30 year T-Bond, and changed the index names to

links, so you can now click on an index to get more individual data.

The E-Mini at the bottom of the table is the S&P 500 equity futures

contract.

|

LAST

|

CHANGE

|

% CHG

|

||

|

|

17740.63

|

79.92

|

0.45%

|

|

|

|

4736.16

|

19.06

|

0.40%

|

|

|

|

2057.14

|

6.51

|

0.32%

|

|

|

|

1114.72

|

6.77

|

0.61%

|

|

|

|

2312.76

|

-0.53

|

-0.02%

|

|

|

|

16193.47

|

86.75

|

0.68%

|

|

|

|

331.67

|

-1.19

|

0.77%

|

|

|

|

6125.7

|

8.45

|

0.08%

|

|

|

|

45.46

|

0.8

|

1.79%

|

|

|

|

45.92

|

0.55

|

1.21%

|

|

|

|

1.766

|

3/32

|

|

|

|

|

2.629

|

0/32

|

|

|

|

|

15.1

|

0.38

|

2.58%

|

|

|

|

2052.75

|

0

|

0.00%

|

The

Saudi’s replaced their long running oil minister Ali al-Naimi as part of

a broad government and economic restructuring, but so far they have not

signaled any change in oil policy. Greece is back in the headlines,

and the battle for Brexit is heating up. There wasn’t much interesting

financial news over the weekend, as politics continues to dominate the

media, and Donald Trump is already backtracking on his vague economic

policies. I do think this article on a Los Angeles based

financial advisor who builds portfolios mostly out of alternative assets is

interesting. He is basically building endowment style portfolios for

individual investors http://bit.ly/AltsZeal.

He must be doing something right, since he manages $1.5 billion in assets and

is ranked by Barron’s as a top independent advisor.

Have a great week, here’s

the news:

|

|

|

|

|

|

Saudi Arabia’s King Salman issued more than 50 royal decrees

on Saturday in a government shake up that sees the oil minister and central bank head

replaced. The changes, the latest step in the Saudi Vision 2030 plan for a

post-oil state, also include a range of measures to encourage foreign

investment in financial markets in the country. Oil producers across the

Middle East are seeking to implement reforms for the longer run but perhaps

more significantly for investors, in the short term they are turning to the bond market to fill

financial holes created by persistently low oil prices.

|

|

|

|

|

|

|

The debate on Britain's membership of the European Union is

set to kick up a gear this week with speeches due from the Chancellor of the

Exchequer, the governor of the Bank of England and the

head of the International Monetary Fund. With about 20 percent of voters

still undecided ahead of the June 23 referendum, there is still much to play

for. U.K. Prime Minister David Cameron, in a speech this morning, evoked the

memory of wartime leader Winston Churchill in a

patriotic appeal to Britons not to vote to leave the EU. The pound - which

has been the developed world's worst-performing currency

this year - is holding its four-day decline against the dollar this morning,

trading at $1.4450 at 5:50 a.m. ET.

|

|

|

|

|

|

|

|

The seemingly never-ending Greek austerity talks are back in

the spotlight today following last night's successful vote in the

country's parliament to implement pension and tax reforms. The euro area and

the IMF will meet today to discuss whether the measures are enough to allow

another disbursement of emergency funds, with the IMF demanding more

fiscal “contingency measures” worth about 3.5 billion euros ($4 billion)

in case Greece strays off budgetary course. The debate

will also focus on the possibility of debt relief for the euro area

member.

|

|

|||||||

|

|

|||||||

|

Equity markets across the world, with the major exception

of China, are generally higher this morning. The MSCI Asia Pacific Index dropped 0.2 percent to 126.94 with the

Shanghai Composite Index doing most of the damage, closing 2.8 percent lower as trade data

released over the weekend disappointed. In Europe, the Stoxx 600 Index was 1.38 percent higher at 5:47 a.m. ET

following German factory orders data that showed a pick up in that economy.

S&P 500 futures were 0.4 percent higher.

|

|||||||

|

|||||||

|

|

|||||||

|

Iron ore prices are getting clobbered once again. The SGX

AsiaClear contract for June settlement in Singapore plunged 9.1 percent.

Meanwhile, spot ore prices in Qingdao just had their worst week since 2011,

and are off over 17 percent from their recent highs. West Texas Intermediate

crude is up close to 2 percent as of 6:16 a.m. ET, amid ongoing wildfires in

Canada that have knocked approximately 1 million barrels of production offline.

In other commodity news, hedge funds are the most bullish that they've been on gold

since 2011.

Saudi Arabia has a new oil boss. Ali al-Naimi is out as the Saudi oil minister after 20 years. The veteran oil minister will be replaced by the chairman of Saudi Arabia's state-owned Aramco, Khaled al-Falih, who has been named head of the newly created Energy, Industry, and Natural Resources Ministry. The shakeup is part of the kingdom's "2030 vision" to diversify away from its dependence on oil. West Texas Intermediate crude oil is up 2.1% at $45.59 a barrel. There are more details on a Saudi Aramco IPO. Ambrose Evans Pritchard of The Telegraph reports that Saudi Arabia is planning to list its oil giant Aramco in Hong Kong, London, and New York in addition to Riyadh. The total listing, which is planned for 2017 or 2018, will value the company at $2.5 trillion. According to Saudi Deputy Crown Prince Mohammad bin Salman, the kingdom will sell just 5% of the oil behemoth. There's a split at the Bank of Japan over negative rates. The minutes from the March BOJ meeting show that policymakers had conflicting views on the central bank's negative-interest-rate policy. The Japan Times reports that the latest minutes showed that a few members had voiced concerns that negative interest rates "had not necessarily exerted its intended effects." Others, however, believed the recent strength in the yen and in Japanese stocks weren't because of policy but were due to "the overly heightened risk aversion of investors worldwide." The Japanese yen is weaker by 0.9% at 108.04 per dollar. Greece passed more reforms. Greek lawmakers approved "unpopular pension and tax reforms" in hopes of securing more bailout cash, according to Reuters. The measures were passed by a slim margin ahead of Monday's Eurogroup meetings. The International Monetary Fund has repeatedly called for a restructuring of Greek debt, but so far there hasn't been any agreement on the matter. German factory orders gain unexpectedly. Factory orders in Germany unexpectedly rose 1.9% month-over-month in March, ahead of the 0.6% gain that was expected. Monday's reading was supported by a 6.2% jump in export orders from outside the euro area. The euro is weaker by 0.1% at 1.1390 per dollar. Berkshire Hathaway misses. The Warren Buffett-led conglomerate announced operating earnings of $2,274 a share, missing the Bloomberg consensus of $2,761. Revenue rose 7.7% to $52.4 billion, but that was shy of the $52.88 billion that was anticipated. Class A shares ended Friday's session at just under $217,000 apiece. Twitter is blocking US spy agencies from using its analytics. The Wall Street Journal reports that Twitter has banned US intelligence agencies from using Dataminr, a service it partly owns that provides real-time alerts for breaking news stories. According to a Twitter representative, the company has "never authorized Dataminr or any third party to sell data to a government or intelligence agency for surveillance purposes," and "this is a longstanding Twitter policy, not a new development." US spy agencies had used the service for two years before the ban was put in place.

Earnings reports continue to flow. JD.com, Teva Pharmaceuticals, and Tyson Foods are among the names reporting ahead of the opening bell. Hertz Global, MBIA, and Solar City are among the companies releasing their quarterly results after markets close.

US economic data is absent. A slow week for economic

data kicks off on Tuesday with the release of JOLTS - Job Openings and

wholesale inventories.

|

The jump in the U.S. dollar catches traders short.

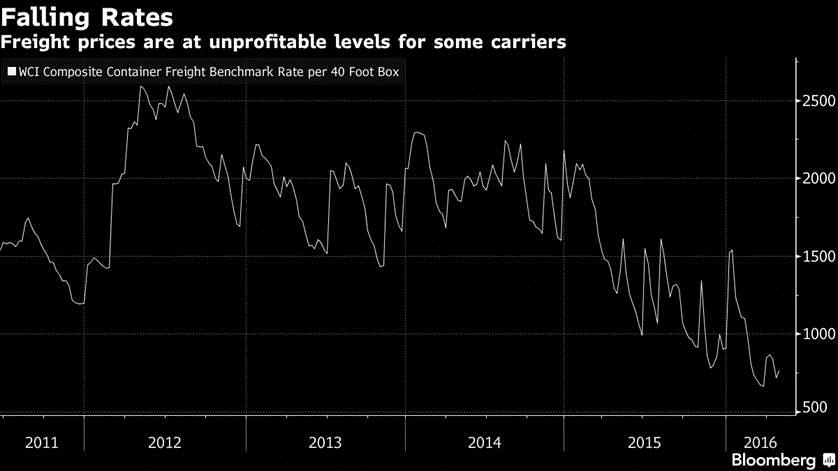

Negative rates hit global shipping.

The guys who created the model for SIVs are back with a

bank.

Years of historically low interest rates have failed to stoke

the inflation that central bankers around the world are so keen to see. Now

the big question is whether negative interest rates (Nirp) will do what low

rates could not accomplish. The CEO of one shipping company offers a hint as

to why central bankers will fail yet again. Nils Smedegaard Andersen, chief

executive officer of A.P. Moeller-Maersk A/S, told Bloomberg that current policy

"means that consolidation will be much slower because it’s easy for

banks to keep weak shipping companies above water.” In other words, too many

shippers are staying alive because of cheap money and that's preventing

industry consolidation and making it harder to get pricing power. Of course

Andersen, as the head of a shipping giant, has his own personal reasons why

he'd like to see more of his rivals go out of business. But his point may

hold - and apply to other industries as well (including oil companies that

might otherwise go bust were it not for continued loans and investment).

Meanwhile, China is arguably continuing to export deflation, so long as its

credit-led stimulus keeps zombie enterprises alive. None of this is to

definitively say that low or negative rates are counterproductive, but it's

interesting to see more examples of how they can produce consequences that

work against stated policy goals. Years of historically low interest rates have failed to stoke

the inflation that central bankers around the world are so keen to see. Now

the big question is whether negative interest rates (Nirp) will do what low

rates could not accomplish. The CEO of one shipping company offers a hint as

to why central bankers will fail yet again. Nils Smedegaard Andersen, chief

executive officer of A.P. Moeller-Maersk A/S, told Bloomberg that current policy

"means that consolidation will be much slower because it’s easy for

banks to keep weak shipping companies above water.” In other words, too many

shippers are staying alive because of cheap money and that's preventing

industry consolidation and making it harder to get pricing power. Of course

Andersen, as the head of a shipping giant, has his own personal reasons why

he'd like to see more of his rivals go out of business. But his point may

hold - and apply to other industries as well (including oil companies that

might otherwise go bust were it not for continued loans and investment).

Meanwhile, China is arguably continuing to export deflation, so long as its

credit-led stimulus keeps zombie enterprises alive. None of this is to

definitively say that low or negative rates are counterproductive, but it's

interesting to see more examples of how they can produce consequences that

work against stated policy goals. |

|

|

Source:

Bloomberg, BI, WSJ, Barron’s

Labels: DailyMarketPrimer, Fed, Investments, Markets, Oil

posted by Rich Barnett @ 7:32 AM

![]()

![]()

0 Comments:

Post a Comment

<< Home